Zeroing Down Zero Cost EMI Schemes

If you're also an avid fan of purchasing electronic goods at 0 cost EMI, but wonder how do the finance companies make money on these schemes, then go on... this post would satiate your inquisitiveness

“Sir double door refrigerator would look good this Diwali at your place. Do not worry about paying now. Just avail the 0 cost EMI scheme and you can pay in easy installments.”

Quoting a recent conversation overheard in one of the electronic stores. For sure, you must have also come across such instances where you purchased a white good or got an offer to purchase something in 0% interest for 6, 12 or 18 months. We have all enjoyed this easy credit facility, but the question which remains unanswered is how do the financing companies make profit on these schemes?

Let’s understand first what a zero cost 0% EMI scheme is?

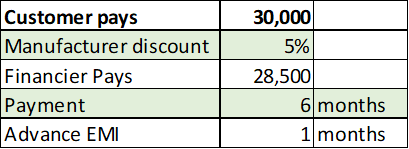

You like a refrigerator of 30,000 rupees. You are dicey whether to purchase the same or not? However, someone offers you a 6-month interest free EMI loan and hence asks you to pay 30000/6 = INR 5,000 per month to take the refrigerator. You become tempted to purchase this at 5,000 upfront cost instead of 30K and suddenly the refrigerator appears to be more affordable for you. And of course, the probability of shopkeeper hearing – “I’ll purchase this next time” - reduces significantly.

Seems like a win-win for both the parties, right?… But who takes the risk of payment of 30K on your behalf? It’s the FINANCIER like your bank or an NBFC and if that entity is ready to take that risk, then definitely it will want something in return because there aren’t any free lunches. So, a simple arrangement works between all the four parties involved in the transaction i.e. the customer, the shopkeeper, the manufacturer and the financier.

- The manufacturer says that if my sale is increasing through this no cost EMI scheme, I’m ready to offer 5% upfront discount on the product (this isn’t passed to the customer though)

- So, the customer now pays 30K, but the financier gives to the manufacturer only 28.5K (5% less than the original price)

- The manufacturer also offers the same commission on the sale of any product which may be 10-15% to the shopkeeper, so the shopkeeper is also happy because this would help in more sales and more commissions.

- Lastly, the financier you may think is the entity losing it all. It pays 28.5K upfront to the manufacturer to get back 30K only after 6 months. That’s just 5% over 6 months or 10% annualized. Sounds too less, right? Then read the next part carefully, which will prove how the financier is actually the real king in this deal.

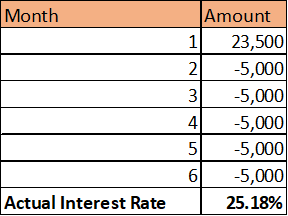

Remember, the financier pays 28.5K to the manufacturer upfront and gets back 30K from you in 6 months. Effectively, he gets back 5,000 in 6 months which includes the principal and some interest every month. What’s this rate of interest? It’s a whopping ~18% interest rate every month. This is because mathematically, the 28,500 goes to zero in 6 months, so the average tenure of the loan is about 3 months and the rest 3 months it’s the interest payment time. Hence, INR 1500 earned in three months on 28,500 is about 5%. So, 3 months and 5% = 12 months and nearly 20% annually.

You may use the IRR function in Excel to calculate the following results yourselves.

So, for any lending institution this works well because the money earned from this scheme is used to give loans to other customers and this deal sweetens even more for the financier if you even pay 1 EMI in advance. 1 EMI doesn’t sound so big a deal but for the financier it’s a whopping 25% interest earnings per annum.

So, this scheme effectively is a win-win for all the parties. In-fact at 25% interest rates, the financier even may pay some extra commission to the shopkeeper to get the products financed through his institution. And if you are thinking what if the customers don’t pay the financier back in time, then it’s a fact that dishonest people are a fraction of what honest people are in this world. Moreover, at 25% interest rate, the risk seems minimal in terms of payoff.

Seems like a masterstroke scheme, isn’t it?

By: Anmol Gupta | Isha Garg

And if you like the explanation of such masterstroke concepts by us in the most simple ways, then don’t forget to subscribe:

gentle feedback and I know for a fact you folks love feedback: maybe putting names of companies will be more exciting and fun and easy to understand for the dumb reader like me. Plus I would love a way to tackle this strategy next time should I ask Rel Digital to give me a direct 10 % discount if I want to take the no-cost EMI thing; cause EMI's do hamper your credit score(Am I right on this one?; fact checked I am wrong multiple loans do not impact credit score until I pay them all on time). Maybe an article on why a credit score is important and myths around it because I did not believe a credit score was important in college(Yes I was one of those bozos who did not take the AMex free card for life) until I saw Frank Abignale on Google Talks<superb talk do check it out>. Great work, super consistency keep going

financier, manufacturer, shopkeeper - too many entities confuse me. Can you dumb it down further for me: in case of lets say offline shopping itself for now: Reliance Digital is the shop keeper ; Icici is the financier; I understand these 2 earning something why is a manufacturer like Samsung concerned. Product I am buying is a Samsung refrigerator worth 30k. Am I missing something that no cost EMI is just on Samsung Refrigerator and not on LG?